Finance Byte - Week 15 Product-Unit Economics

Table of Contents

- Recap

- Product-Based Unit

- Summary Steps

- Increase Contribution Margin

- Systems

Recap

During Week 14, we introduced the topic of unit economics. What is Unit Economics?

Unit Economics describes a specific business model's revenues & costs in relation to an individual unit. A unit refers to any basic quantifiable item that creates value for a business.

So, in simple terms, it is about identifying the smallest unit responsible for creating value for a business or from where a business earns it's revenues.

We then explained why is unit economics important?

Understanding unit economics in terms of margins & costs allows businesses to :

- Identify profitable products

- Optimize pricing &

- Ensure long-term sustainability of the business

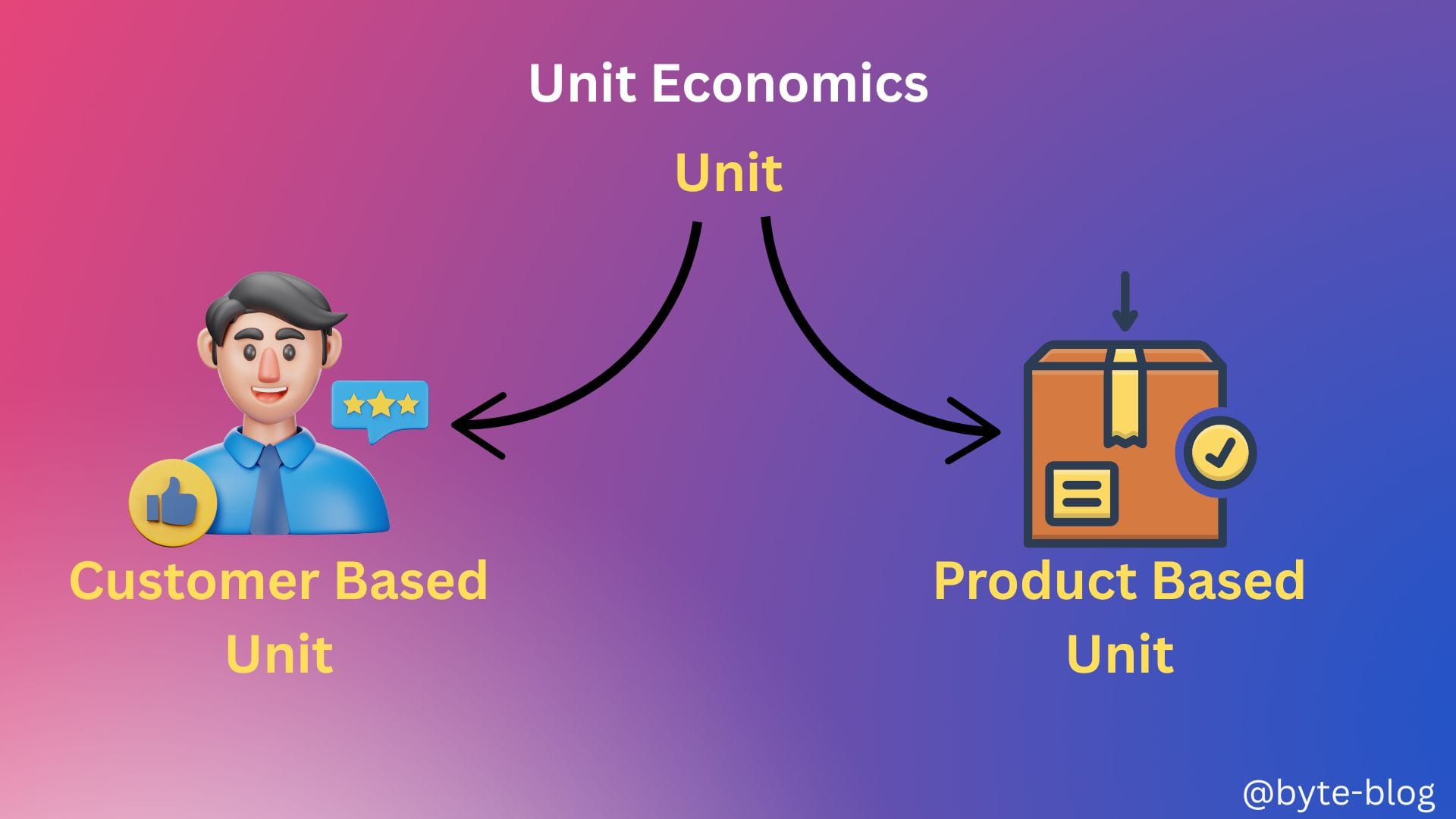

We moved forward & defined a "unit" & classified it broadly under two heads :

- Product-based unit

- Customer-based unit

Product-based Unit

Here, the "unit" under analysis is a single product. Unit economics at the product level focuses on

- Direct Revenues through pricing &

- Unit Costs associated with producing / manufacturing & selling a single unit of a product.

In very simple terms, it is measuring revenues from a single product vs. cost of producing & selling that product.

Customer-based Unit

Here, the "unit" under analysis is a single customer. Unit economics at a customer level focuses on

- Direct Revenues &

- Costs

associated with acquiring, serving & retaining a single customer.

In very simple terms, it is measuring revenues from a single customer vs. cost of acquiring & maintaining that customer. E.g., Banking Services & Netflix are two examples where customer based unit economics is used.

This week, we deep dive into Product-based unit economics.

Product-Based Unit

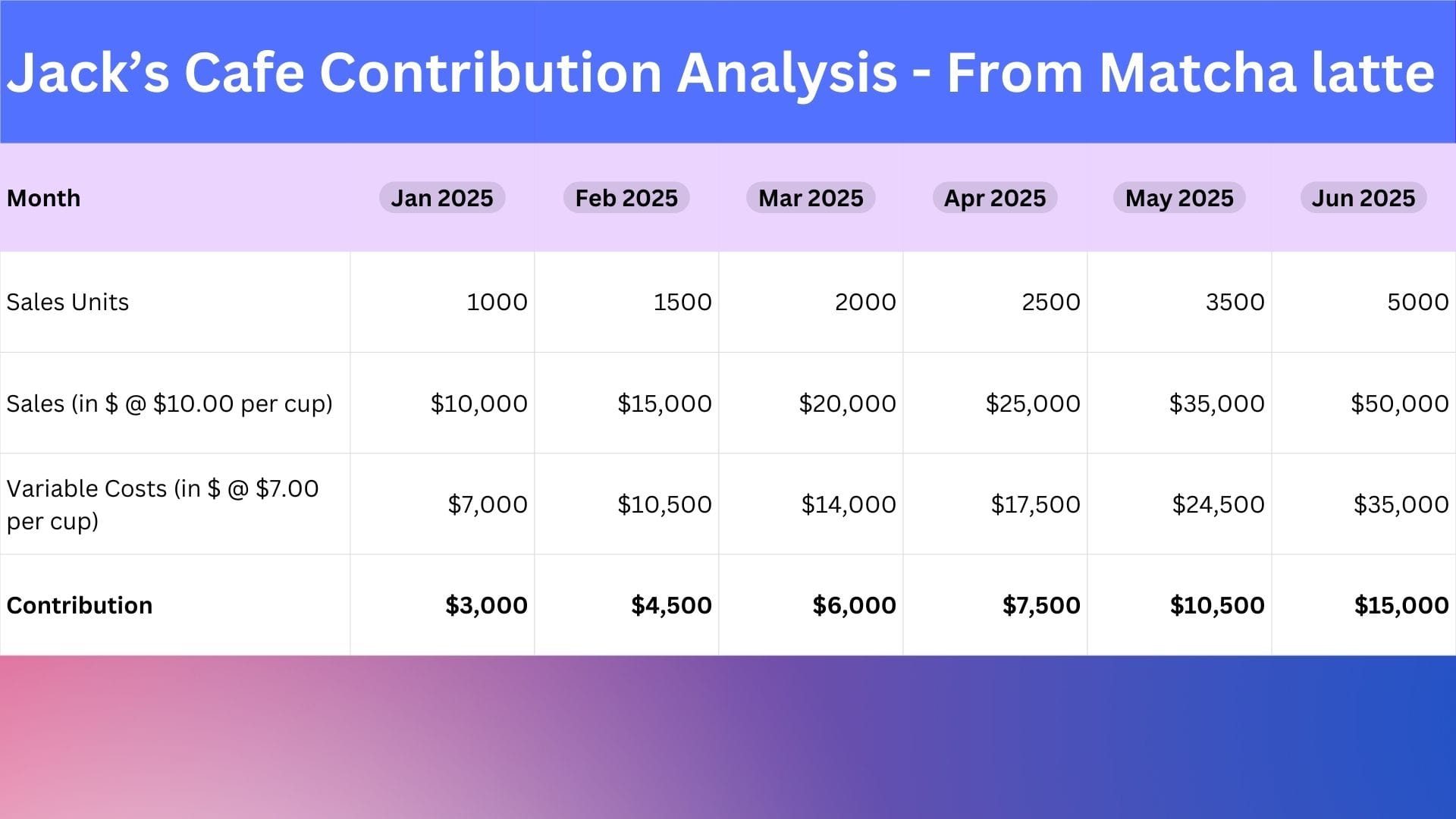

Let us use Jack's Matcha Latte to explain product based unit economics.

Over the last couple of weeks, we helped Jack identify his unit economics for each cup of Matcha Latte by

- Considering revenue per cup of Matcha Latte through pricing &

- Identifying variable costs per unit

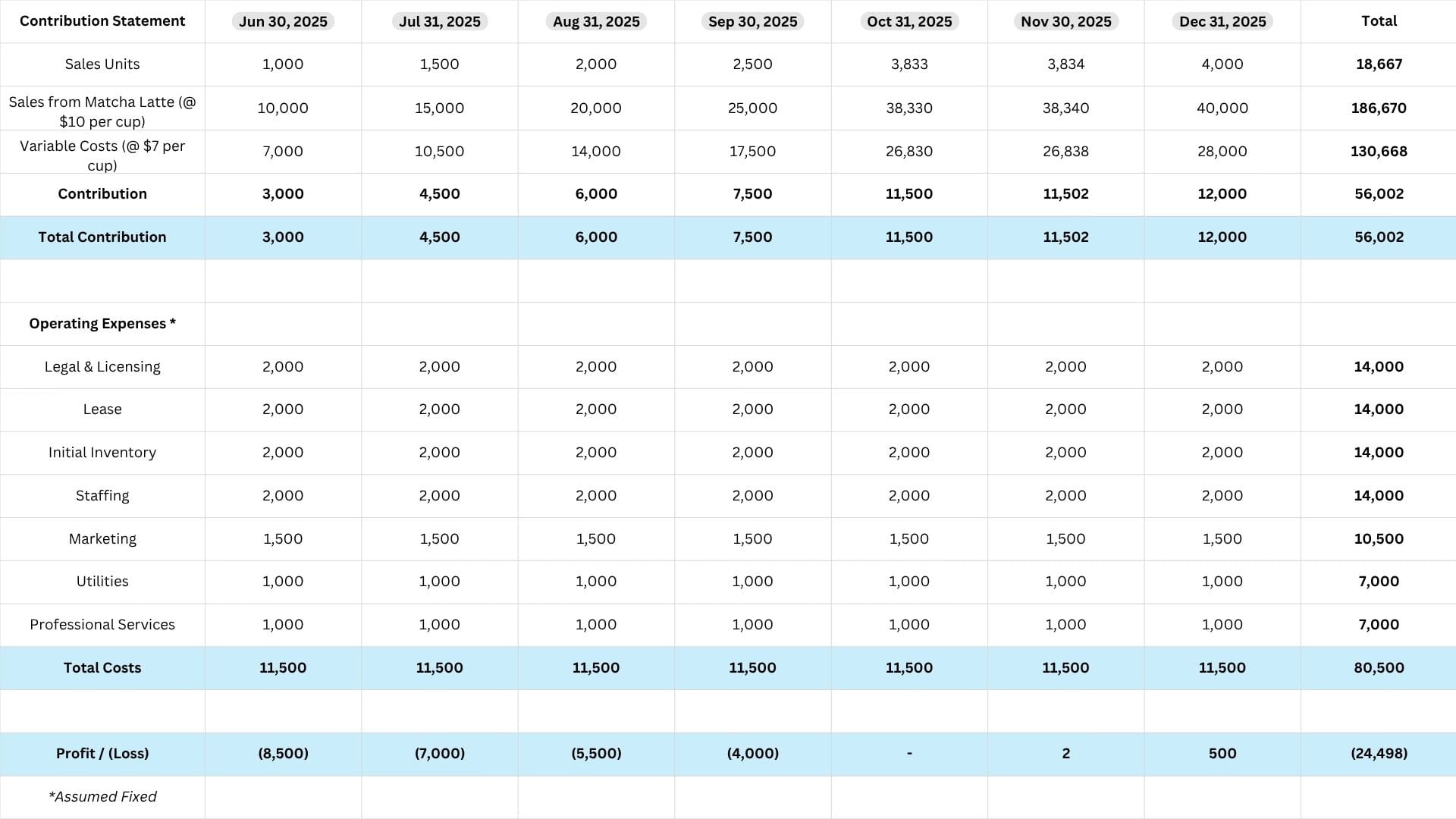

Multiplying the difference between the two by units sold, we arrived at total contribution as visualized below:

With this analysis,

- Jack understands how much he needs to price his coffee to cover variable costs plus make a margin in line with market.

- After that, he can identify how many units of each product he needs to sell to cover fixed costs.

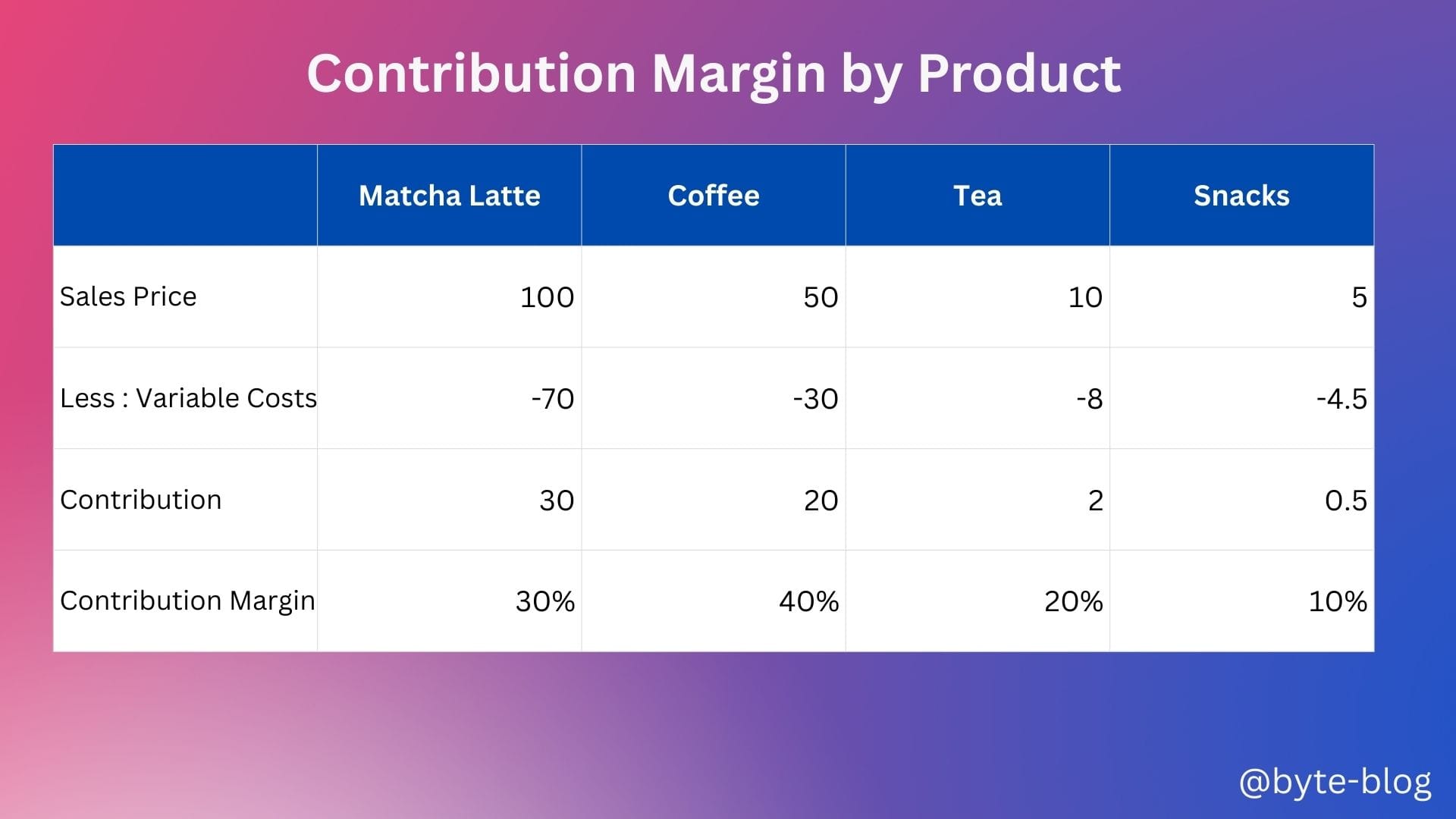

If he has multiple products,

The product with highest contribution margin requires the least volume of sales to cover fixed costs or will cover fixed costs faster compared to sales of products with lesser contribution margin. For e.g., Jack breaks even at 3,833 units of Matcha Latte at 30% contribution margin. He will need higher volumes of tea or snacks to cover the same level of fixed costs as their contribution margin is lower than that of Matcha Latte.

Assuming he sells only Matcha Latte, he breaks even at 3,833 units after which he generates profit compared to loss at 2,500 units.

Let us summarize the above step by step :

Summary Steps

Step 1 - Identify the unit

Here, Jack's unit is a cup of coffee or a single unit of any other product (snacks, tea etc).

Step 2 - Calculate Revenue Per Unit

Jack sells one cup of Matcha Latte at $10. This is his revenue per unit.

Step 3 - Determine Variable cost Per Unit

Jack's accounting system was parametrized to determine variable costs for one cup of Matcha Latte at $ 7.

Step 4 - Calculate Contribution

Contribution is (Revenue per unit - Variable Cost per unit)

Step 5 - Identify Breakeven Point

Identify how much unit sales at a particular contribution margin would cover the fixed costs? The exact point at which total sales covers the fixed cost or where profit is zero is the breakeven point & the minimum sales needed to avoid loss.

Break Even Point = Fixed Costs / Contribution per unit

We can conclude that

If Contribution > Fixed costs, the net result is operating profits &

If Contribution < Fixed costs, the net result is operating loss

So, all this analysis is good. But what actionable steps Jack can take to increase his contribution margin? Let's go action next...

Increase Contribution Margin

How do you think Jack can increase his contribution margin? He can do so by

- Increasing the pricing of his products

- Reducing costs (Variable & Fixed)

- Optimizing Product Mix

Let us explore them in detail.

1) Increase Pricing

In our example above, Jack was selling a cup of Matcha Latte at $10. If he increases the pricing to $15, his contribution (assuming variable costs remain the same), will be

$15 - $7 = $8 instead of

$10 - $7 = $3, an increase of $5.

This would result in higher contribution from sales & increase in operating profits.

But, can he actually increase his price just like that? No.

This is where market pricing comes to play. The price of a similar Matcha Latte in another cafe might cost $10 or $12. He can only increase his pricing up to what the market & competition allows.

Any price over & above that will be rejected by the customers & Jack will be forced to bring down his price to bring back the demand for his product.

But if he does something, maybe the price increase is justified & that is when he increases the value to customer.

2) Reduce Costs

To make a cup of Matcha Latte, Jack spends around $7. This $7 consists of

- cost of raw materials,

- labor costs &

- any other costs which move in line with production &/or sales.

Jack can talk to his vendors & negotiate with them to reduce material costs in line with purchases. For e.g., the suppliers can reduce their pricing for higher purchase volumes.

Or, he can automate some processes to minimize manual processes &/or labor reducing costs &/or improving efficiency. Here also,

by reducing input cost or improving efficiency, he increases value to customer by reducing waiting time &/or costs which in turn results in higher contribution margin.

But, what is value?

3) Value

I will pick the definition from an excellent & highly recommended book "Monetizing Innovation" by Madhavan Ramanujam.

Value is defined as the perceived value that a product holds for a customer, which directly influences their willingness to pay.

How can Jack increase value to his customers? For e.g., by including an ingredient which makes the latte taste better which in turn increases it's value in the eyes of the customer. In such cases, customers will be willing to pay higher amount for the latte.

Or if Jack adds a Matcha cookie which goes well with the Matcha Latte & sells it as a bundle at a higher price, that increases value to customer who will pay higher prices willingly for the combo offer.

On the cost side, Jack can reduce the cost factor (willingness to supply) by negotiation with vendors &/or increasing effficiency.

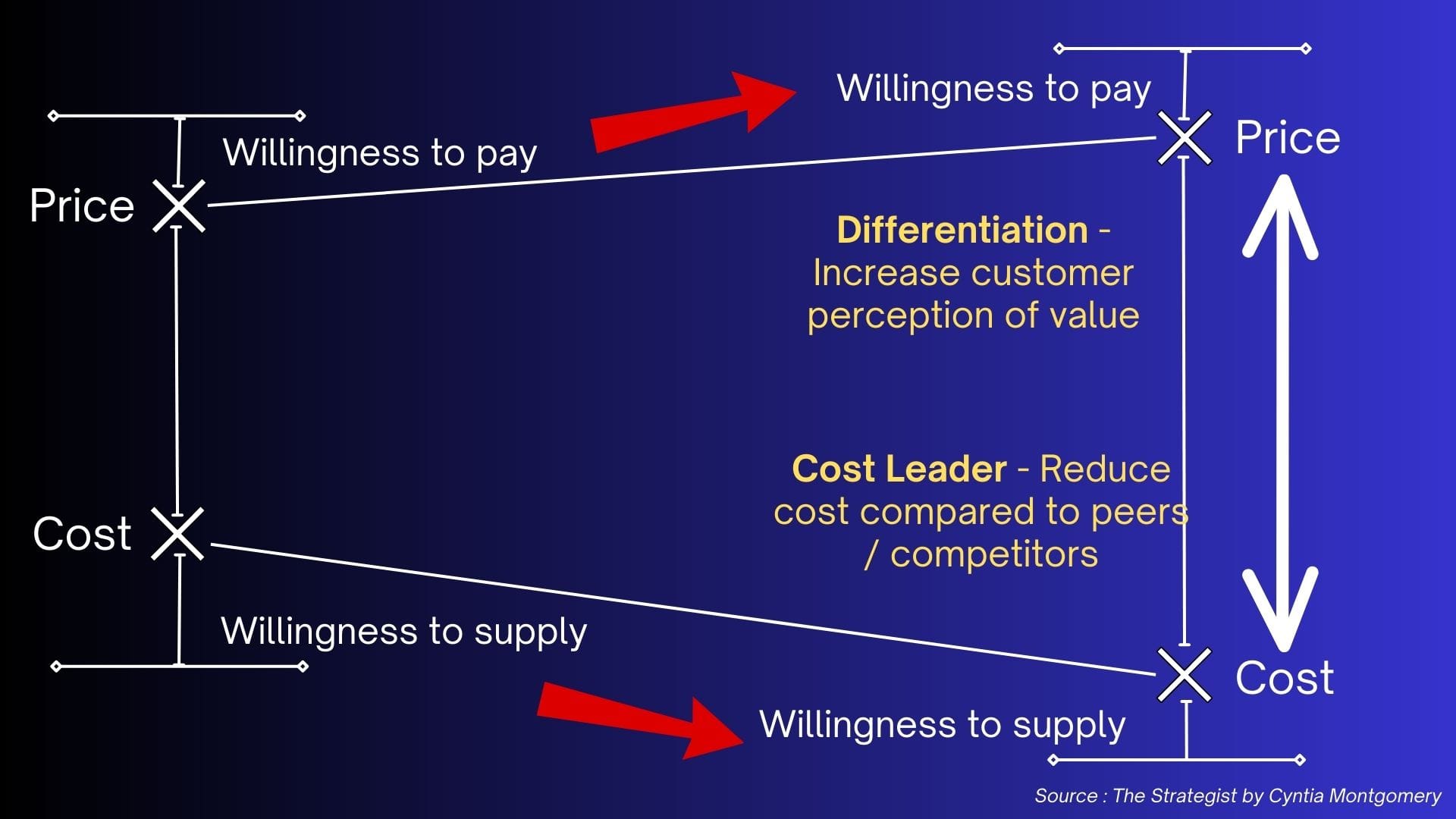

This reminds me of a visual I shared in Week 6 of Strategy Bytes. See how the price point & cost moves from left to right.

By increasing value, Jack ensures that his customers keep coming back & maybe refer new customers which will result in higher sales.

As he nets higher sales with more customers, he can negotiate with his vendors for pricing discounts which will further reduce his variable costs increasing his contribution margin.

He can introduce or improve efficiencies in fixed costs by investing in automation.

4) Optimizing Product Mix

He can optimize his product mix by selling more of high margin products & only include other low margin products to satisfy customer demand while maximizing his profit potential.

Systems

For getting granular cost & revenue information by individual unit, Jack has to invest in good systems to identify & classify costs to individual units. That is another ocean to explore by itself.

Next week, we will discuss customer-based unit economics.