Strategy Byte - Week 36 Demand

Recap

During Week 35, we discussed at a high level the concepts of Market & Price.

A market is any place or venue where buyers & sellers can exchange goods & services.

Then we defined Competitive Market as a market where there are a large number of buyers & sellers where no single buyer or seller can influence the price of goods being sold.

Then we moved on to Price & classified it as :

- Money Price &

- Relative Price

Money price is the amount of currency that is given up in exchange for that good or service.

Relative price is the price of one item relative to another.

With limitation of resources (money), there are trade offs involved in our day to day decisions to spend money. In other words, resources are allocated to ensure most efficient utilization in line with our preferences.

We described relative pricing as a useful concept to help consumers & producers make informed decisions about resource allocation to spend or produce a product or service in line with demand. But what is Demand ?

Let us now explore Demand

Demand

Demand is : The desire or need of customers for goods or services that they want to buy or use. (Source : here).

So, if we demand a good or service, it means that we want it. But then, it is not enough that we want something. Why? As we mentioned last week, there are constraints around resources & in this case, that resource is money.

With limited money, there are constraints around what we can afford even though we may want something or there is a demand for that item. Thus, we should be able to afford that good or service.

Thus affordability is a key factor in demand. For e.g., a consumer may want a Lamborghini. So, there is a demand. But not all can afford a Lamborghini.

Assuming we can afford the item that we want, we should have a plan to buy it. If we don't have a definite plan to buy something, then we cannot say that there is a demand for that item.

So there are three aspects to demand :

- There should be a want for a good or service

- The good or service should be affordable &

- There should be a plan to buy that good or service

With limited resources or in other words - Scarcity, not all our wants will be satisfied. Based on the trade-offs, demand reflects the decision about which "wants" will have to be satisfied based on our preferences at that point in time.

There are two variables used to measure demand. They are :

- Quantity

- Price

The quantity demanded of a good or service is the amount that customers plan to buy during a time period. It is normally measured as an amount per unit of time.

The price is the amount at which the quantity demanded is bought or purchased.

Let us now delve into what drives demand & the factors affecting it.

Factors Affecting Demand

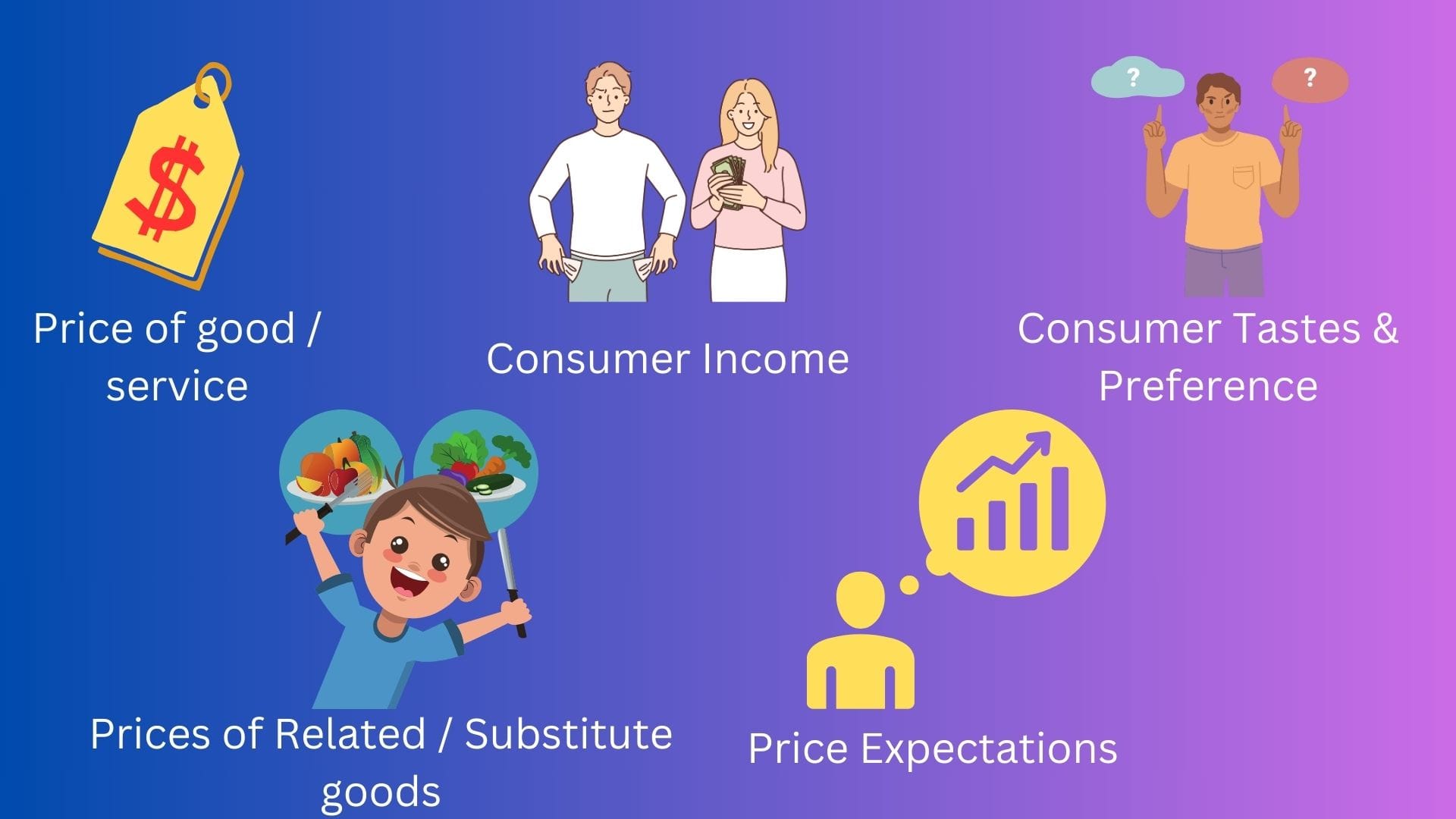

There are five factors which drive demand :

- Price of good / service

- Consumers' Income

- Consumers' tastes & preferences

- Prices of related or substitute goods

- Expectations of Price

Representing the above visually :

Let's explore each of the above factors:

Price of Goods / Service

As I mentioned above, affordability is key when deciding whether to buy a good or service. Lambhorgini is manufactured for a particular customer segment (which is very narrow) who can afford one (or many!!).

The production & demand for Lambhorgini reflects this customer base while the demand for a Toyota or any other model reflects the broader customer base who can afford a Toyota or other models.

Consumers' Income

Continuing from the above, affordability is a direct consequence of

- The income earned by an individual consumer &

- Whether they are able to spend the required amount to purchase that good or service.

If the price of a good or service rises relative to consumers' income, they cannot afford to buy that more expensive good or service. Hence, demand for that good or service falls.

Consumers' Preferences

Consumer preferences change over a period of time & across generations. Fashion industry is a good example of changes in demand depending on consumer tastes & preferences.

Goods which are out of fashion will see lesser demand while newer trends will have higher demand.

Price of Related Goods & Services

We discussed buying oranges & apples last week. Assuming the relative price of oranges rise, it's opportunity cost which means the sacrifice that a consumer makes if he/she doesn't buy those oranges also rises.

If apples provide almost the same benefits, apples can substitute oranges and hence people will buy more apples & less oranges or in other words, as the opportunity cost of a good rises, people buy less of that good & more of its substitutes.

Another example we can think of is streaming subscriptions. If Netflix increases their subscription, there would be a set of consumers who might go for Disney+ or HBO Max which provide similar services. Or Apple Music vs. Spotify and so on..

Price Expectations

If the price of a good or service is expected to rise in the future, the opportunity cost of obtaining the good or service for future use is lower today than it will be when the price has increased.

So consumers time their purchases accordingly & buy more of that good (assuming the goods can be stored) or service now before it's price is expected to rise, so the demand for the good or services increase now.

Conversely, if the price of a good or service is expected to fall in future, the opportunity cost of buying the good or service now is high relative to what it is expected to be in the future.

So, consumers time their purchase & buy less of the good or service now before it's price falls. So the demand for the good or service decreases today & increases in the future.

Thus, there are multiple variables at play driving demand of a good or service. However behind the scenes, there is a pattern driving the inter-play of these variables. Next week we will look into these patterns under

- Law of Demand &

- Demand Curve