Strategy Byte - Week 38 Supply

Table of Contents

- Recap

- Supply

- Law of Supply

- Supply Determinants

Recap

During Week 37, we discussed Law of Demand as :

Other things remaining the same, if the price of a good or service increases, it's demand falls & vice versa.

Then we explored

- Substitution Effect - where people substitute the product or service (whose price increased) with a substitute product

- Income Effect - where income levels of consumers remain the same while the prices of goods / services increases. Hence, consumers will spend less resulting in lower demand

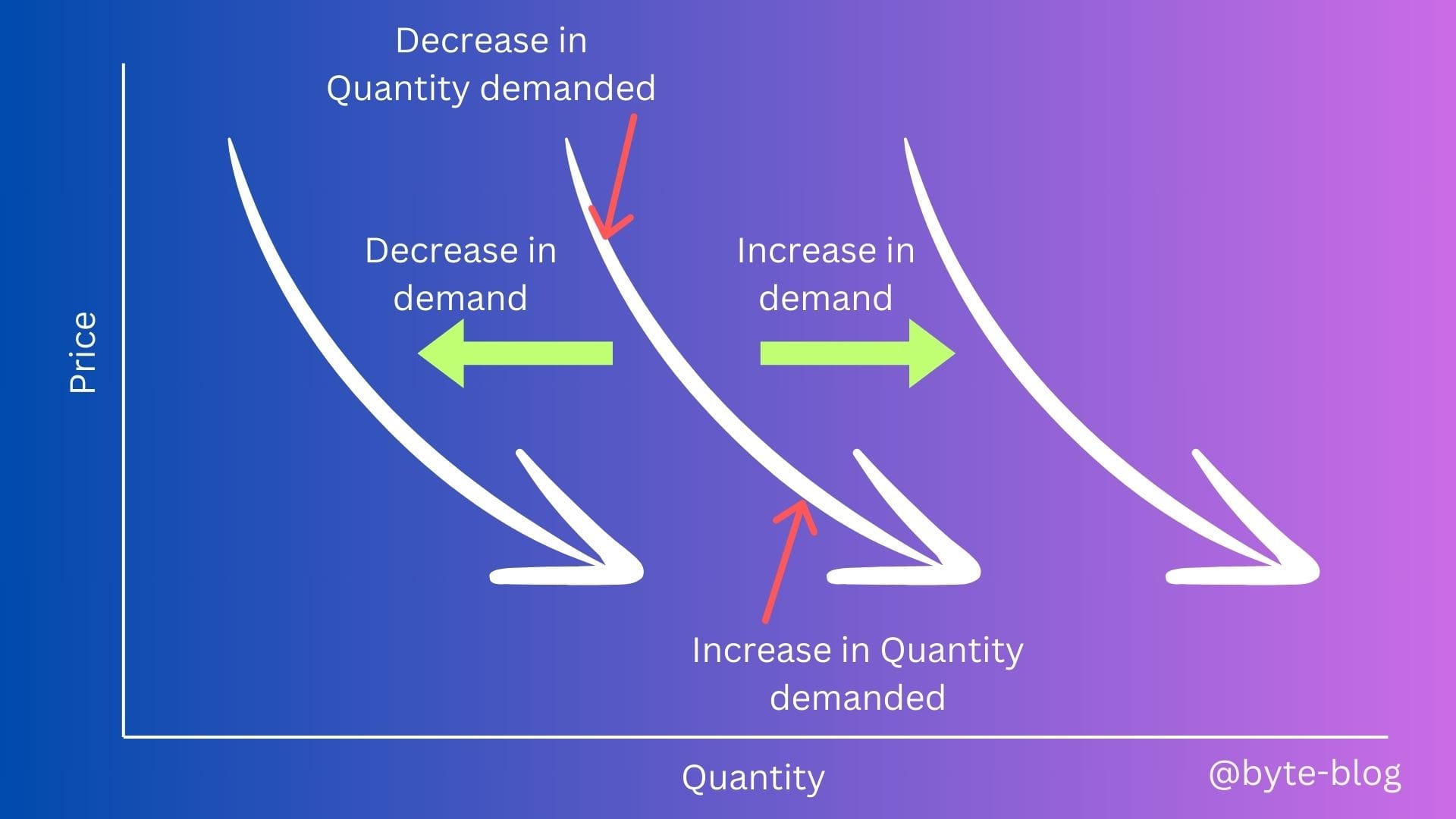

We discussed Demand Schedule & Demand curve which shows the relationship between price & demand & Change in Demand.

When any factor that influences buying plans other than the price of goods / services, it causes a change in demand visualized as below:

Next we discussed Elasticity of Demand which measures how demand responds to a change in price or income.

If price change or any other factor leads to a significant change in demand for goods / services, it is referred to as Elastic Demand otherwise it is referred to a Inelastic demand.

The sum total of all individual demand curves = Industry Demand Curve

Let us now explore Supply which is the other side of demand.

Supply

Before we get into the formal definition of supply, what does it mean?

It means a firm or a person is producing something - can be a good or service. Now why should that firm or person produce a good or service?

- Because they have the resources to produce it &

- They can monetize the product or service by selling it at a particular price.

Simple, right? With the above in mind, let us define supply

Supply is a term in economics that refers to the number of units of goods or services a supplier is willing & able to bring to the market for a specific price. (Source : here)

So, if a firm supplies a good or service, the firm

- Should have the resources to produce that good or service

- can profit from producing & supplying that good or service

- has a definite plan to produce & sell that good or service

Now, is the above enough? No....

To be able to sell a good or service which has been produced at a particular price, there has to be demand for that good or service at that price. Thus, price is a key factor in determining supply of that good or service and that in turn depends on the demand for that good or service. Thus, both supply & demand are inter-linked and balance each other.

Visualizing the above,

Just like Demand, there are two variables used to measure supply. They are :

- Quantity &

- Price

Quantity

In economics, quantity supplied describes the number of goods or services that suppliers will produce & sell at a given market price. (Source : here).

Like quantity demanded (discussed during Week 36), quantity supplied is also measured as an amount per unit of time.

Price

The definition of Price is the same as that we discussed during week 36 as below:

The price is the amount at which the quantity demanded is bought or purchased

Law of Supply

On the demand side, we explored the relationship between quantity & price through the Law of Demand.

Like demand, there are many factors which influence supply & one of them is price. How does price impact the supply of a good or service? Let us understand through the Law of Supply.

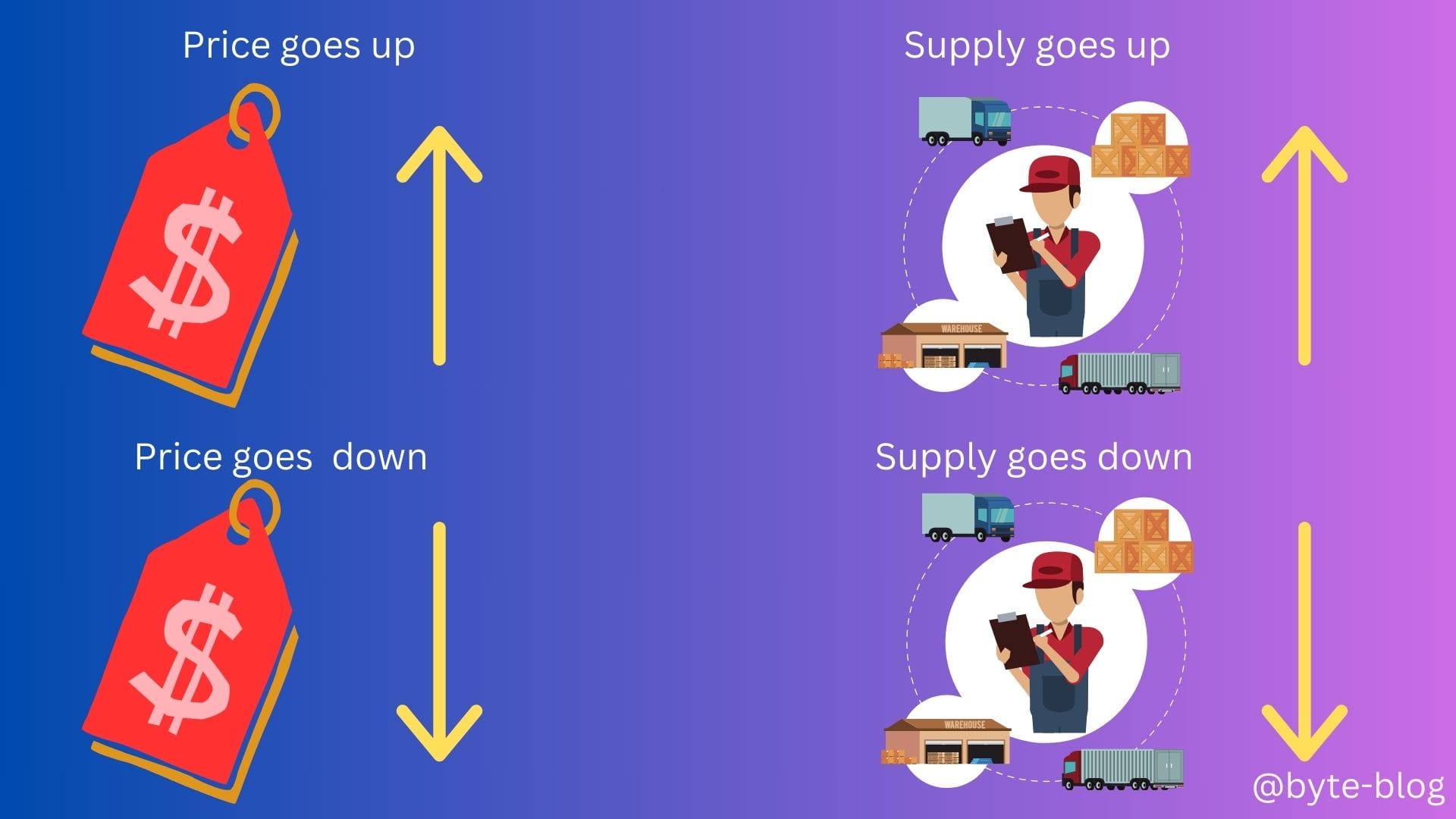

Other things remaining constant, an increase in the price of a good or service leads to an increase in the quantity supplied, while a decrease in price results in a decrease in the quantity supplied. (Source : here)

Visualizing the above:

Now, why do you think this happens?

Let us put ourselves in the producers' shoes. Other things being equal, what will happen if they produce more of the goods or services? They have to incur additional costs for each new good produced.

If these goods can be sold at a higher price that would cover this additional cost incurred for producing that additional good plus earn their margin, the producers or suppliers would gladly increase production. This additional cost is called marginal cost of producing that good or service.

If the prices of goods fall down, producing additional goods will only increase their marginal costs bringing their margin down & increasing losses. Hence, decreasing supply will help them avoid losses.

In other words, other things being equal, if the higher price covers the marginal cost of production plus gives a good margin, then producers are more than willing to increase production. (Refer to visualization below under Cost of Production)

But is price the only determinant of supply? Let us see.

Supply Determinants

In reality, there are multiple factors determining supply of a good or service. These are :

- Cost of Production

- Prices of related goods

- Expected future prices

- No. of Suppliers

- Technology & Innovation

Let us explore each of the above

Cost of Production

When the cost of production of a good or service rises, a firm decreases their production or supply to reduce losses. Why? Because at the same price & higher cost of production, the margin or profit on sale of an additional good decreases. Let us visualize it below :

A good which costs $ 500 to produce is sold at $ 1,000 resulting in a margin or profit of $ 500.

If the cost of production increases from $ 500 to $700 without any increase in price, the profit or margin from that good reduces from $ 500 to $ 300. Increasing production in such a scenario would increase losses or reduce profit of the firm.

Prices of related goods or services

The prices of related products can affect the supply of a particular product. For e.g., if the price of tyres increase, it impacts the price or supply of bicycles where bicycle manufacturers either have to increase their price or reduce supply.

Expected future prices

If the price of a good is expected to increase in the future, the return from selling the good in the future is higher than it is today. So, firms decrease supply today & plan to increase it in the future to take advantage of future price increase.

No. of Suppliers

The no. of suppliers in the market also influences the supply. When there are more suppliers, the overall supply tends to increase as each new supplier contributes to the market supply.

Technology & Innovation

In this fast moving age of automation & AI, technological innovations can lead to improved production processes & higher efficiency resulting in lower cost &/or higher supply. New technological advancements enable suppliers to produce more goods at lower cost.