Strategy Byte - Week 72 - IMF WEO Report Analysis

Table of Contents

- Introduction

- Before the War

- Impact of War - Global Growth Forecast

- Impact of War - Inflation Forecast

- Medium Term Outlook

- Risks to Outlook

- Rare Earths & Oil Disruption

I was about to move forward to the next phase of our Strategy Journey with industry analysis when I came across this report from IMF World Economic Outlook Report for April 2026 (Link to Report : here).

IMF releases this report regularly but there are two factors that caused me to pause & reflect on this report :

- We were exploring key macro economic variables & how changes to these variables need to be considered when formulating or keeping track of WWHTBT (What Would Have To Be True) conditions in strategy &

- The outbreak of war in the Middle East is not just change in macro-economic variables but the whole equation itself is under stress. So, Central banks, governments & companies need to reframe their actions not only in line with ongoing events in the economy but also manage the stress arising from the war.

So I thought I will go through this report in terms of what we discussed over the last couple of weeks & how this situation changes the economic trajectory that we were going through & the outlook.

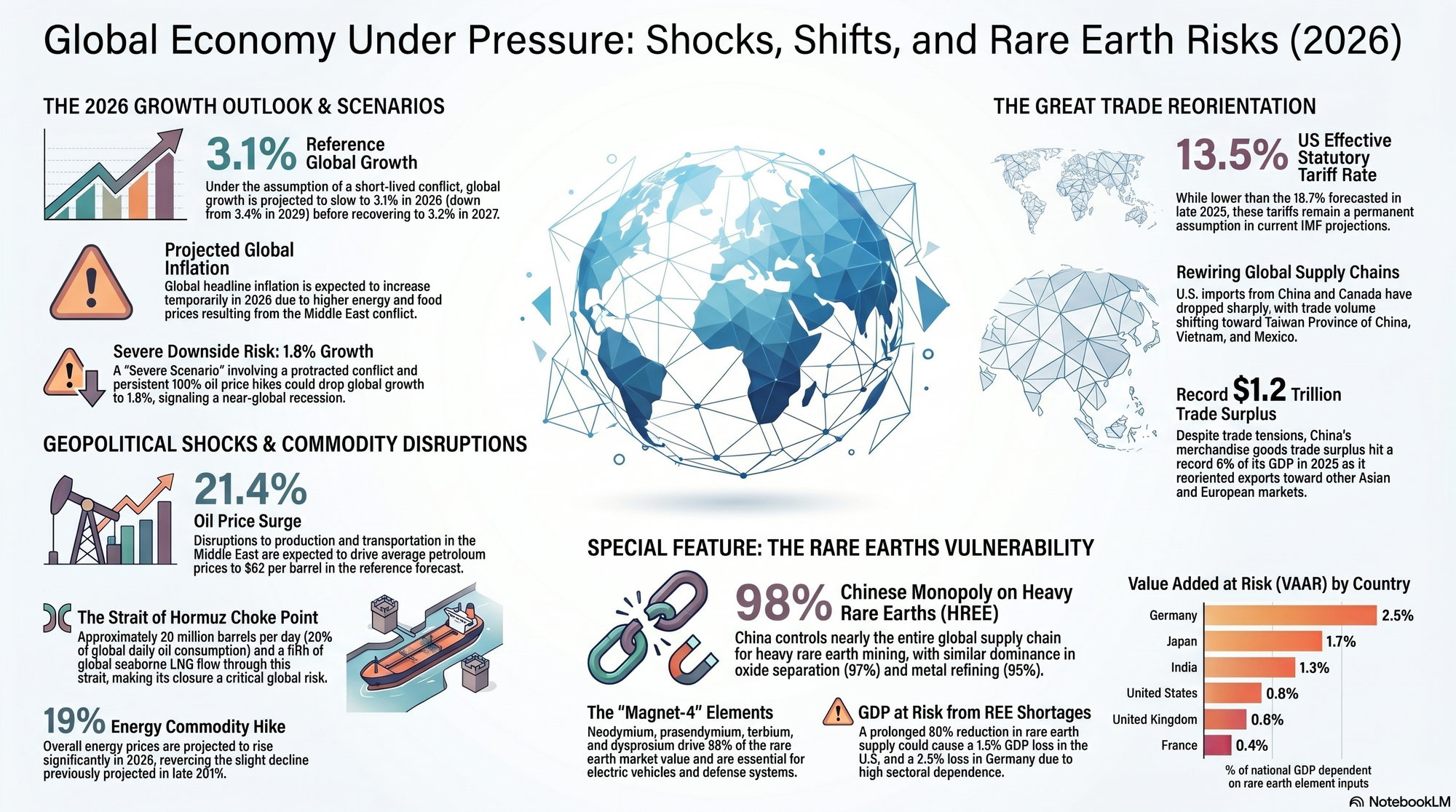

The below visual (using NotebookLM) provides a high-level view of the key points discussed below :

Before the War

We start with the conditions before the war as a starting point for our discussion :

- The world economy has withstood a series of shocks over the last couple of years like Russia-Ukraine war, imposition of US trade tariffs, conflicts surrounding Rare Earth minerals, etc. But the global economy was generally resilient against these events.

- However, the Middle East conflict since the end of February is testing this resilience.

- The global economic impact will crucially depend on the conflict's duration, intensity & scope - which are inherently unpredictable.

- Before the war, the global economy was performing better than expected, laying the groundwork for upward revisions to forecasts.

- In aggregate, global growth in the fourth quarter of 2025 increased to 3.9% on an annualized basis.

- Global trade remained robust with brisk expansion in technology related exports offset slowing momentum in exports in other product categories.

- Rewiring of global supply chains & trading relations continued amid imposition of US trade tariffs in 2025. US imports from China dropped sharply; those from Canada also declined. These dips were offset by increases in imports from Taiwan , Vietnam, and, to a lesser extent, Mexico.

- On the other side of the equation, Chinese exports were reoriented from the United States to other Asian economies and, temporarily, to Europe. China’s merchandise goods trade surplus hit a record $1.2 trillion (6 percent of GDP) in 2025.

- Global inflation has been largely steady. Concerns about a resurgence of inflation have raised bond yields and driven equity prices down.

Impact of War - Global Growth Forecast

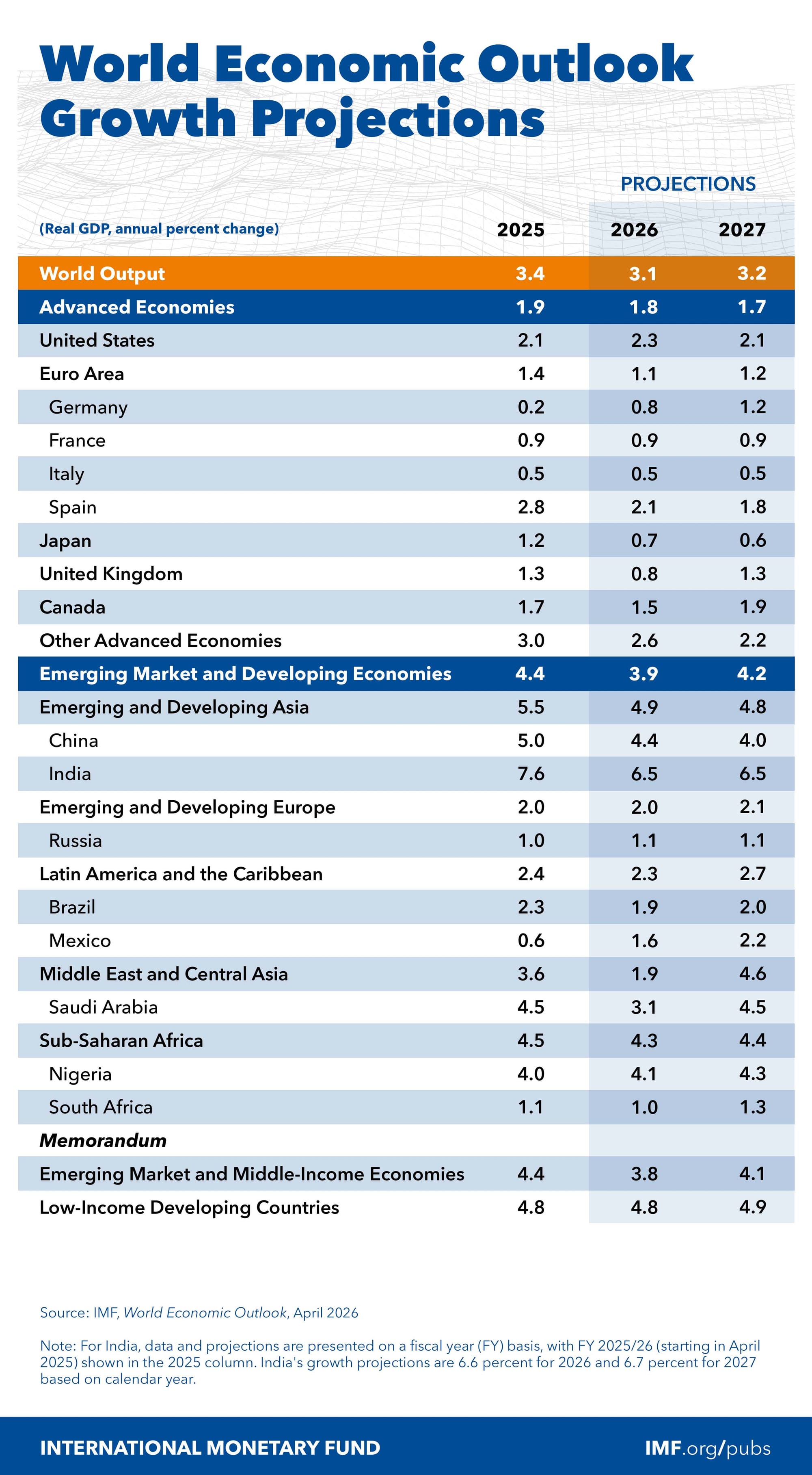

The report projects growth across three potential scenarios depending on the duration & severity of the ongoing Middle East conflict :

- Reference Forecast - Predicated on a relatively short-lived conflict, this baseline scenario anticipates that global growth will slow down modestly to 3.1% in 2026 & 3.2% in 2027. This forecast marks a deceleration from the estimated 3.4% achieved in 2025

- Adverse Scenario - Assuming a more prolonged conflict that spikes oil prices by 80% & gas prices by 160%, global growth would reduce by 0.8% points down to 2.5% in 2026 before reaching 3.0% in 2027

- Severe Scenario - Under the severe scenario, global growth would reduce by 1.3% points in 2026, dragging the global growth rate to below 2%, bringing the world dangerously close to a global recession & to 2.2% in 2027.

The country-wise breakup of the growth under various scenarios is visualized below :

With slower growth as articulated above, how would inflation fare under each scenario?

Impact of War - Inflation Forecast

Under each scenario articulated above, the forecasted inflation is :

- Reference Forecast - Global headline inflation is projected to temporarily increase to 4.4% in 2026 - up from 4.1% in 2025, largely due to anticipated higher food & energy prices. It is then expected to fall back to 3.7% in 2027.

- Adverse Scenario - Driven by significant spikes in oil & gas prices, global inflation would be 1.5% points higher than the baseline, reaching 5.4% in 2026.

- Severe Scenario - In the event of a severe, persistent commodity shock, inflation would be 190 basis points higher, reaching 5.8% in 2026. This inflationary pressure would worsen over time, pushing inflation 260 basis points higher to reach 6.1% in 2027.

So, the deadly cocktail of slower growth & higher inflation is called stagflation. This situation is like a double edged sword & problematic because typical policy tools to fight inflation (higher interest rates) can further suppress growth and jobs, while tools to stimulate growth (lower rates, fiscal expansion) can worsen inflation.

Medium Term Outlook

- Many countries are facing challenges in lifting medium-term growth prospects compounded by geo-economic fragmentation & rising geopolitical risks.

- The global economy is projected to expand at an average annual pace of 3.1% in 2028-31, compared to pre-pandemic (2000-19) historical average of 3.7%.

Risks to Outlook

Downside Risks include :

- Further intensification of conflicts and eruption of domestic political tensions: The current war and geopolitical tensions could intensify further, food security could be threatened, and erosion of real incomes could exacerbate external imbalances and put countries with limited reserves at risk of balance of payments distress and social unrest. - We covered Balance of Payments in great detail. It records all a country’s transactions with the rest of the world and helps assess its external strength. Countries with weak external balances (large deficits, low FX reserves, and limited access to foreign currency) face greater risk of not being able to finance essential imports

- Reevaluation of productivity gains from new technology: Should AI-driven profitability projections turn out to be overly optimistic, real investment in technology sectors could drop sharply, and equity markets could be vulnerable to a sharp repricing.

- Disruption of the fragile balance of current trade policies: More countries could adopt a protectionist posture, and sector-specific tariffs or nontariff measures targeting critical inputs might also disrupt global supply chains.

- Erosion of confidence in economic institutions: Intensification of political pressure on independent central banks and other policy institutions can erode hard-won public confidence and lift inflation expectations.

- Repricing of borrowing costs triggered by fiscal vulnerabilities: Public debt is elevated in several major economies, and fiscal sustainability worries could put pressure on borrowing costs, tighten broader financial conditions, and amplify financial market volatility.

This point was discussed last week where we pointed out higher debt to GDP ratio of US at 123.3%. Borrowing more than a country's productivity engine (GDP) raises the risk of default & is exacerbated due to the current geopolitical events. It's like having high credit card debt when we don't have the means to repay them.

US public debt is projected to continue climbing significantly, rising from 124 percent of GDP in 2025 to 142 percent in 2031

The debt-to-GDP ratio in the euro area is also expected to rise, though at a much slower pace than in the US, increasing from 87 percent in 2025 to 90 percent in 2031.

Public debt across Emerging Market & Developing economies is projected to rise steadily, reaching 86 percent of GDP in 2031, up from 74 percent in 2025.

Upside Risks include

- Faster materialization of productivity gains from artificial intelligence,

- Accelerated implementation of structural reforms, and

- Tangible progress in trade talks.

We will touch upon certain commodities which have outsized impact on economies due to their usage in key industrial products & services.

Rare Earths & Oil Disruption

- Oil prices increased 57.6 percent between August 2025 and March 2026 to $105.8 per barrel as a result of the military conflict in the Middle East. Middle East supply disruptions also put upward pressure on European and Asian natural gas prices.

- Rare earth elements (REEs) supply chains are structurally vulnerable. China maintains 88 percent of the world’s oxide separation capacity and 93 percent of its metal refining for light REEs, and retains a near monopoly across the entire global supply chain for heavy REEs.

- Large disruptions to REE supplies could substantially reduce GDP in many economies, and model-based analysis suggests that de-risking supply chains through targeted industrial policies is fiscally costly.

It is important to understand the first & second order effects of such events on your company's business & financial position to take necessary action to safeguard key assets, liquidity etc.